Finance & Stock Market learnings

06 Jul 2025Read educational articles online from Zerodha Varsity, Upstox, Groww, Smallcase followed folks on Youtube/Twitter/WebArticles, asked doubts to GPT etc., and wrote below notes.

In this article I will write about my learnings around indian stock market, fundamental & technical analysis of stocks, etc., which I have been doing for some months. Although, work keeps me busy, I try my best to keep track of the markets and rotate my finances whenever necessary.

Table of Contents

- Table of Contents

- Market Fundamentals

- Market Jargon

- Investment Instruments

- Technical Ratios and Metrics

- Tax Saving Strategy

- Futures Options

- Other Info

Market Fundamentals

Market Structure and Infrastructure

Stock Exchanges

India operates two primary stock exchanges that form the backbone of its capital markets:

- Bombay Stock Exchange (BSE): Established in 1875, it’s Asia’s oldest stock exchange and home to the benchmark Sensex index

- National Stock Exchange (NSE): Founded in 1992, it’s India’s largest exchange by trading volume and hosts the popular Nifty 50 index

Both exchanges operate under strict regulatory oversight and provide electronic trading platforms for seamless transactions.

Market Participants

The Indian stock market ecosystem comprises diverse participants, each playing a vital role:

Individual Investors

- Domestic Retail Participants: Individual investors like retail traders and long-term investors

- Non-Resident Indians (NRIs) and Overseas Citizens of India (OCIs): People of Indian origin residing abroad who can invest through designated channels

Institutional Investors

- Domestic Institutions: Corporate entities and organizations based in India

- Domestic Asset Management Companies (AMCs): Mutual fund companies such as SBI Mutual Fund, HDFC AMC, ICICI Prudential, and Axis Mutual Fund

- Foreign Institutional Investors (FIIs) and Foreign Portfolio Investors (FPIs): International entities including foreign asset management companies, hedge funds, pension funds, and sovereign wealth funds

Regulatory Framework

The Securities and Exchange Board of India (SEBI) serves as the market regulator, ensuring:

- Fair and transparent trading practices

- Investor protection

- Market integrity and stability

- Compliance with prescribed rules and regulations

SEBI continuously updates regulations to align with global best practices and protect investor interests.

Market Intermediaries and Account Structure

Essential Intermediaries

Your journey in the stock market involves three key intermediaries:

1. Stockbrokers

Your gateway to market access, stockbrokers enable you to:

- Buy and sell stocks, bonds, ETFs, and mutual funds

- Access research and market insights

- Provide trading platforms and tools

- Offer advisory services

2. Depositories

Financial intermediaries offering Demat (Dematerialized) account services:

- National Securities Depository Limited (NSDL)

- Central Depository Services (India) Limited (CDSL)

Both operate under SEBI regulations with virtually no functional differences. The Demat account holds your securities in electronic format, replacing the old paper certificate system (pre-1996).

3. Banks

Provide the bank account for fund transfers and settlements.

The Three-Account System

Successful trading requires three interconnected accounts:

- Trading Account: Provided by your broker for placing orders

- Demat Account: Offered by depository participants for holding securities

- Bank Account: For fund transfers and settlements

All three accounts operate electronically and are seamlessly integrated for smooth transactions.

Clearing and Settlement

NSE Clearing Limited and Indian Clearing Corporation (ICCL) are wholly-owned subsidiaries of NSE and BSE respectively. These clearing corporations ensure guaranteed settlement of all trades, providing counterparty risk protection to investors.

Market Timings and Sessions

Understanding market timings is crucial for effective trading and investment decisions.

Pre-Opening Session (9:00 AM - 9:15 AM)

This session sets the stage for the trading day through three distinct phases:

Order Entry Period (9:00 AM - 9:08 AM)

- Place, modify, or cancel orders for any securities

- Orders placed during this time receive priority when trading begins

- Beneficial for strategic positioning before market opens

Price Discovery (9:08 AM - 9:12 AM)

- No new orders or modifications allowed

- System determines opening prices through multilateral order matching

- Matches buy and sell orders based on demand and supply

- Critical for establishing fair opening prices

Transition Period (9:12 AM - 9:15 AM)

- Buffer time between pre-opening and normal trading

- No new orders allowed

- Existing orders cannot be modified or cancelled

- System prepares for normal trading session

Normal Trading Session (9:15 AM - 3:30 PM)

The primary trading session where:

- All regular transactions occur

- Bilateral order matching system operates

- Real-time price discovery based on demand and supply

- Maximum market liquidity and activity

Post-Closing Session (3:30 PM - 4:00 PM)

Closing Price Calculation (3:30 PM - 3:40 PM)

- Closing prices calculated using weighted average of prices from 3:00 PM - 3:30 PM

- Benchmark indices (Nifty, Sensex) closing values determined

- Important for next day’s reference pricing

After-Market Orders (3:40 PM - 4:00 PM)

- Place orders for next day’s trading

- Orders execute at predetermined prices regardless of next day’s opening

- Provides opportunity for price discovery after regular hours

- Orders can be cancelled during early pre-opening session (9:00 AM - 9:08 AM) if needed

Special Trading Sessions

Muhurat Trading: Despite being generally closed on Diwali, the market opens for one ceremonial hour during this auspicious festival, allowing investors to make symbolic investments.

Types of Market Participants by Trading Style

Day Traders

- Initiate and close positions within the same trading day

- Do not carry positions overnight

- Focus on short-term price movements

- Require active monitoring and quick decision-making

Scalpers (Subset of Day Traders)

- Hold positions for very short periods (minutes to hours)

- Trade large volumes for small but quick profits

- Require excellent timing and market understanding

Swing Traders

- Hold positions for several days to weeks

- Capitalize on medium-term price movements

- Less time-intensive than day trading

- Focus on technical patterns and trends

Long-term Investors

- Hold positions for months to years

- Focus on fundamental analysis

- Benefit from compounding and dividend income

- Less affected by short-term market volatility

Order Types and Trading Strategies

Understanding different order types is essential for executing your investment strategy effectively.

Basic Order Types

Market Order

- Executes immediately at the best available market price

- Higher probability of execution

- Price may vary from expected due to market movements

- Example: Placing order for ₹100 might execute at ₹105 (higher) or ₹95 (lower)

Limit Order

- Executes only at specified price or better

- Lower probability of execution

- Provides price certainty

- Example: Limit order at ₹100 will only execute at ₹100 or favorable price

Stop Loss Order

- Triggered when stock reaches predetermined price level

- Limits losses or protects profits

- Two variants:

- Stop Loss Market (STM): Converts to market order when triggered (higher execution probability)

- Stop Loss Limit (STL): Converts to limit order when triggered (execution not guaranteed)

Advanced Order Types

Cover Order

- Combination of buy order with automatic stop loss

- Provides built-in risk management

- Formula: Cover Order = Buy Price + Stop Loss

Bracket Order

- Most comprehensive order type

- Includes entry, stop loss, and target price

- Formula: Bracket Order = Buy Price + Stop Loss + Target Price

- Automatically exits position at either stop loss or target

After Market Order (AMO)

- Orders placed after market closure

- Executed when market reopens next day

- Price difference possible between order placement and execution

- Useful for capturing overnight news impact

Immediate-or-Cancel (IOC) Order

- Must execute immediately or get cancelled

- Partial execution possible

- Example: Order for 100 shares might execute 60 shares, cancel remaining 40

Day Order vs. Good-Till-Cancelled (GTC)

- Day Order: Valid until end of trading day

- Good-Till-Day: Valid until specified day

- Good-Till-Cancelled: Valid until manually cancelled or expiry date

Delivery vs. Intraday Trading

Delivery Trading

- Shares transferred to your Demat account

- Suitable for long-term investment

- Full payment required upfront

- Dividend and corporate action benefits

Intraday Trading

- Positions squared off same day

- No share delivery

- Margin trading available (leverage)

- Higher risk due to leverage

- Lower capital requirement initially

Clearing and Settlement Process

Understanding the settlement cycle is crucial for planning your trades and managing cash flows.

T+2 Settlement Cycle

T Day (Trade Day)

- Transaction execution day

- Money debited from account immediately

- Shares not yet in Demat account

- Broker generates contract note (transaction bill)

- All charges and taxes applied

T+1 Day

- Exchange processes the transaction

- Shares still not in Demat account

- BTST/ATST Trading Possible: Can sell shares bought previous day (high risk)

- Risk: If original seller defaults, you face auction penalty (up to 20% of stock value)

T+2 Day

- Final settlement day

- Shares credited to Demat account

- Money settlement completed

- Transaction officially closed

T+3 Day

- Shares available for trading without restrictions

- Full ownership rights activated

Important Note: Bank or depository holidays on T+2 may delay settlement, but shares still appear in T1 holdings.

Corporate Actions

Corporate actions significantly impact your investments and require understanding for informed decision-making.

Dividends

Companies share profits with shareholders through dividend payments.

Dividend Process Timeline

- Dividend Declaration Date: Board approves dividend at Annual General Meeting (AGM)

- Record Date: Company reviews shareholder register (typically 30 days after declaration)

- Ex-Dividend Date: Set two business days before record date due to T+2 settlement

- Payment Date: Actual dividend distribution

Key Concepts

- Cum-Dividend: Trading with dividend rights (before ex-date)

- Ex-Dividend Impact: Stock price typically drops by dividend amount on ex-date

- Eligibility: Must own shares before ex-dividend date to receive dividend

Example: If ITC trading at ₹335 declares ₹5 dividend, price drops to approximately ₹330 on ex-date.

Bonus Shares

Free additional shares given to existing shareholders in fixed ratios.

Common Ratios

- 1:1: One bonus share for every share held

- 2:1: Two bonus shares for every share held

- 3:1: Three bonus shares for every share held

Benefits

- Increases shareholding without additional cost

- Makes shares more affordable for retail investors

- Maintains proportional ownership

Stock Split

Increases number of shares while proportionally reducing share price.

Mechanism

- 2-for-1 Split: Each share becomes two shares at half the price

- Face Value Reduction: Reduces in same proportion as split

- Market Capitalization: Remains unchanged

Reverse Stock Split: Combining shares (negative indicator for company health)

Rights Issue

Opportunity for existing shareholders to buy additional shares at discounted price.

Features

- Offered below market price

- Maintains proportional ownership if fully subscribed

- Can be traded, renounced, or partially exercised

- Similar to secondary IPO for existing shareholders

Share Buyback

Company repurchases its own shares from the market.

Benefits

- Reduces shares outstanding

- Potentially increases share price

- Shows management confidence

- Returns excess cash to shareholders

- Improves financial ratios like EPS

Investment Considerations and Tax Implications

Financial Year and Tax Structure

India’s financial year runs from April 1st to March 31st, affecting your tax planning.

Important Terminology

- Financial Year (FY): Year in which income is earned

- Assessment Year (AY): Year in which taxes are filed

- Example: FY 2023-24 income filed in AY 2024-25

Tax Participation Context

Only about 5% of India’s 130+ crore population files income tax returns, with less than 1.5% actually paying income tax. This compares to over 45% in developed economies like the USA, highlighting the growth potential of India’s formal economy.

Alternative Investment Avenues

Commodity Markets

India offers robust commodity trading through multiple exchanges:

Major Commodity Exchanges

- Multi Commodity Exchange (MCX): Largest commodity exchange

- Intercontinental Exchange (ICE): International commodity platform

- National Commodity and Derivatives Exchange (NCDEX): Agricultural commodities focus

- National Multi Commodity Exchange (NMCE): Regional commodity trading

Commodity Categories

- Metals: Gold, silver, copper, aluminum, zinc

- Energy: Crude oil, natural gas, heating oil

- Agricultural: Wheat, rice, sugar, cotton, spices

- Others: Industrial commodities and rare earth materials

Derivatives Market

Futures and Options (F&O)

- Advanced instruments for hedging and speculation

- Require margin payments instead of full amount

- Higher leverage and risk

- Suitable for experienced investors

Market Jargon

Basic Trading Terms

Position Management

Square Off: The action of closing an existing position by executing an opposite transaction. Think of it as completing a trade cycle - if you bought shares, you square off by selling them, and vice versa.

Long Position: When you buy and hold securities expecting their price to rise. You’re “long” on optimism about the asset’s future performance.

Short Position: When you sell securities you don’t own (borrowed through your broker) expecting their price to fall. You profit when you can buy them back at a lower price to return to the lender.

Price Reference Points

Last Traded Price (LTP): The most recent price at which a stock was traded. This gives you a real-time snapshot of market valuation and serves as the starting point for your next trade decision.

52-Week High/Low: The highest and lowest prices a stock has reached in the past year. These levels often act as psychological barriers and reference points for investors to gauge whether a stock is expensive or cheap relative to its recent history.

All-Time High/Low: The highest or lowest price a stock has ever reached since it began trading. Breaking these levels often signals significant market events or company developments.

OHLC Data: Open, High, Low, and Close prices that summarize a stock’s price movement during a specific time period (day, week, month). This data helps you understand the trading range and price volatility, forming the basis for technical analysis.

Trading Mechanisms

Volume: The number of shares traded during a specific period. High volume often indicates strong interest and conviction in price movements, while low volume suggests uncertainty or lack of interest.

Upper Circuit/Lower Circuit: Price bands set by exchanges that limit how much a stock can move up or down in a single trading session. These circuits prevent extreme volatility and give investors time to react to news. When a stock hits an upper circuit, it can only move up to that level, and when it hits a lower circuit, it cannot fall below that price.

Market Conditions and Sentiment

Bull and Bear Markets

Bull Market: A period of rising prices and optimistic investor sentiment. Like a bull that attacks by thrusting upward, prices move higher. Bull markets are characterized by strong economic fundamentals, high employment, and investor confidence.

Bear Market: A period of declining prices and pessimistic sentiment. Like a bear that attacks by swiping downward, prices fall. Bear markets typically involve economic uncertainty, rising unemployment, and widespread selling pressure.

Financial Performance Metrics

Company Fundamentals

Topline: A company’s total revenue or sales figures, appearing at the top of the income statement. This represents the company’s ability to generate business and market share.

Bottomline: The net profit after all expenses, taxes, and costs have been deducted from revenue. This appears at the bottom of the income statement and represents the actual money the company earned for shareholders.

Earnings Per Share (EPS): Net profit divided by the number of outstanding shares. This metric helps you understand how much profit each share represents. A higher EPS generally indicates better profitability per share, but it should be compared with industry peers and historical performance.

Stock Performance Indicators

Alpha: Measures how much a stock outperforms or underperforms compared to a benchmark index like Nifty or Sensex. A positive alpha means the stock performed better than the index, while negative alpha indicates underperformance.

Beta: Measures a stock’s volatility relative to the overall market. A beta of 1 means the stock moves in line with the market, above 1 indicates higher volatility, and below 1 suggests lower volatility than the market.

Investment Strategies and Concepts

Trading Approaches

Momentum Investing: A strategy that involves buying securities showing upward price trends and selling those showing downward trends. This approach assumes that trends will continue in the short term, riding the wave of market sentiment.

Tax Gain/Loss Harvesting: A strategic approach to minimize tax liability by timing the sale of investments. For gains, you can sell investments just before they exceed the tax-free threshold and reinvest immediately to reset the cost basis. For losses, you can book losses to offset future gains, effectively reducing your tax burden.

Investment Returns

Dividends: Regular payments companies make to shareholders from their profits. Think of dividends as your share of the company’s success. There are two ways to earn from investments: capital appreciation (stock price increase) and dividend income (regular payments).

Capital Appreciation: The increase in an investment’s value over time. This represents the difference between what you paid for an asset and its current market value.

Taxation Framework

Capital Gains Tax Structure

Long Term Capital Gains (LTCG) Tax: Applied to profits from stocks held for more than one year. Long-Term Capital Gains (LTCG) on shares and equity-oriented mutual funds in India are taxed at a 12.5% rate (plus surcharge and cess) if they reach Rs. 1.25 lakh in a fiscal year.

Short Term Capital Gains (STCG) Tax: Applied to profits from stocks held for one year or less. Currently, short term capital gains on shares are taxed at a rate of 20% under Section 111A with effect from 23 July 2024.

Dividend Taxation

Since April 2020, dividends are taxed as per your income tax slab rather than being tax-free.

Monetary Policy and Economic Indicators

Interest Rate Framework

Repo Rate: The rate at which the Reserve Bank of India lends money to commercial banks. When RBI increases repo rates, borrowing becomes expensive, reducing money supply and potentially slowing economic growth. Stock markets typically react negatively to repo rate increases.

Reverse Repo Rate: The rate at which RBI borrows money from banks. This tool helps RBI absorb excess liquidity from the banking system.

Cash Reserve Ratio (CRR): The percentage of deposits that banks must maintain with RBI. Higher CRR reduces money available for lending, tightening liquidity in the economy.

Banking Metrics

Credit to Deposit Ratio (CD Ratio): Measures how much of banks’ deposits are being lent out. A higher ratio indicates aggressive lending, while a lower ratio suggests conservative banking practices. This affects credit availability and economic growth.

Economic Health Indicators

Inflation: The sustained increase in general price levels. India typically targets inflation around 4-6%. Moderate inflation indicates healthy economic growth, while high inflation erodes purchasing power and can negatively impact stock markets.

Index of Industrial Production (IIP): Measures the performance of India’s industrial sector, including manufacturing, mining, and electricity. It provides insights into economic activity and industrial growth trends.

Purchasing Managers’ Index (PMI): A leading indicator of economic health based on surveys of purchasing managers in manufacturing and services sectors. A PMI above 50 indicates expansion, while below 50 suggests contraction.

Consumer Price Index (CPI): Measures inflation by tracking changes in prices of goods and services consumed by households. This directly impacts interest rate decisions and monetary policy.

Government Securities and Safe Investments

Treasury Bills

Short-term government securities with maturities of 91, 182, or 364 days. These are considered the safest investments as they’re backed by the government. They’re sold at a discount to face value and redeemed at full value, with the difference representing your return.

Example: A 91-day treasury bill with face value ₹120 might be available at ₹118.40. After 91 days, you receive ₹120, earning ₹1.60 as profit.

Understanding Market Indices

What is an Index?

A stock index represents a group of shares that collectively indicate the performance of a sector, exchange, or economy. Think of it as a representative sample that tells you how the overall market is performing.

Examples:

- Nifty 50: Represents the top 50 companies by market capitalization on NSE

- Sensex: Represents 30 large-cap companies on BSE

- Bank Nifty: Represents banking sector performance

Indices serve as benchmarks for mutual funds and help investors understand market trends without analyzing individual stocks.

Understanding IPOs

-

What is an IPO: Initial Public Offering marks a private company’s transformation into a public entity, allowing anyone to buy shares through stock exchanges

-

Why Companies Go Public:

- Financial reasons: Raise capital without debt, avoid interest payments, get better valuations than private funding

- Strategic benefits: Spread risk across thousands of shareholders instead of few large investors, increase brand visibility and customer trust

- Stakeholder liquidity: Early investors (VCs, PE funds) get exit opportunity, employees can monetize ESOPs

- Growth currency: Use shares for acquisitions and expansion

The IPO Process

- Step 1 - Hiring Merchant Bankers:

- Companies appoint Book Running Lead Managers (BRLM) like Goldman Sachs, Kotak, ICICI Securities

- These bankers handle due diligence, documentation, pricing, and marketing

- Large IPOs may have multiple lead managers

- Step 2 - Regulatory Filing:

- Submit registration statement to SEBI

- Prepare Draft Red Herring Prospectus (DRHP) containing business model, 3-year financials, risk factors, use of proceeds, management details

- Wait for SEBI approval before proceeding

- Step 3 - Marketing Phase:

- Conduct roadshows where management presents to institutional investors

- Launch media campaigns in newspapers, TV, digital platforms

- Generate analyst coverage and research reports

- Step 4 - Price Discovery:

- Set price band (e.g., ₹100-120 per share)

- Open book building process where investors bid within range

- Determine cut-off price based on demand

- Step 5 - Subscription & Allotment:

- Keep bidding window open for 3-5 days

- Collect bids through brokers and banking apps

- Allocate shares via lottery in oversubscribed issues

- Return unallotted money within 6 days

- Step 6 - Listing Day:

- Shares begin trading on NSE/BSE

- Listing price determined by market demand-supply

- Can list at premium, par, or discount to issue price

IPO Pricing Explained

- Key Price Points:

- Face Value: Nominal value (₹1, ₹2, ₹5, or ₹10)

- Issue Price: Face value + Premium charged by company

- Price Band: Range for bidding (lower and upper price)

- Cut-off Price: Final issue price after book building

- Listing Price: First traded price on exchange

- Example Calculation:

Face Value: ₹10 Price Band: ₹485-500 Your Bid: ₹500 (cut-off) Final Issue Price: ₹498 Listing Price: ₹547 Your Gain: ₹49 per share (9.8%) - Grey Market Premium (GMP): Unofficial premium in unlisted market, indicates expected listing gains but can be manipulated

Share Allocation Rules

- Investor Categories & Reservation:

- Retail (RII): 35% reserved for applications up to ₹2 lakhs

- Non-Institutional (NII): 15% for applications above ₹2 lakhs

- Institutional (QIB): 50% for mutual funds, insurance companies, banks

- Oversubscription Impact:

- 2x oversubscribed: Proportionate allotment (get half of applied quantity)

- 10x+ oversubscribed: Lottery system for minimum lot

- Under-subscribed: Full allotment guaranteed

- Primary vs Secondary Market:

- Primary: IPO subscription period, fixed price, money goes to company

- Secondary: Post-listing exchange trading, fluctuating prices, investors trade among themselves

Critical IPO Terms

- Issue Types:

- Fresh Issue: New shares created, funds go to company

- Offer for Sale (OFS): Existing shareholders selling, funds go to them

- Mixed: Combination of both fresh and OFS

- Special Features:

- Green Shoe Option: 15% extra shares can be issued if oversubscribed

- Anchor Investors: Large institutions investing before public opening

- ASBA: Application Supported by Blocked Amount - money blocked, not debited

- Lock-in Period: Promoters can’t sell for 3 years, anchors for 30-90 days

- Application Process:

- Apply at cut-off to maximize allotment chances

- Use UPI for amounts up to ₹5 lakhs

- Multiple applications allowed using different PAN cards

- Avoid last-day rush due to technical glitches

Red Flags & Investment Strategy

- Warning Signs:

- Company using IPO funds primarily for debt repayment

- Negative cash flows with no profitability roadmap

- Valuations significantly higher than industry peers

- High OFS component indicating existing investors exiting

- Complex corporate structures or high related-party transactions

- For Listing Gains:

- Monitor GMP trends but don’t rely solely on them

- Check QIB subscription as institutional interest indicator

- Smaller issues often give higher listing pops

- Have clear exit strategy on listing day

- For Long-term Holdings:

- Study DRHP thoroughly, especially risk factors

- Compare valuations with listed competitors

- Understand revenue model and growth drivers

- Research promoter background and execution track record

Reality Check

- Performance Statistics: Only 50-60% of IPOs deliver positive listing gains. First-month post-listing typically volatile. Sector timing often matters more than company quality. Hyped IPOs don’t always make best long-term investments.

- Common Investor Mistakes: FOMO-driven applications without research. Over-allocating portfolio to IPO investments. Ignoring fundamentals while chasing listing gains. Depending entirely on grey market premiums.

- Portfolio Perspective: Treat IPOs as portfolio diversification tool, not core strategy. Best companies often list at fair valuations and grow steadily.

Investment Instruments

Traditional Banking Products

Fixed Deposits (FDs)

Fixed Deposits represent the foundation of conservative investing in India. When you invest in an FD, you’re essentially lending money to a bank for a predetermined period at a guaranteed interest rate. Think of it as a promise from the bank - they guarantee to return your principal plus interest after the agreed timeframe.

Key Features:

- Guaranteed Returns: Interest rates typically range from 4-7% annually, depending on the bank and tenure

- Safety: Deposits up to ₹5 lakh are insured by the Deposit Insurance and Credit Guarantee Corporation (DICGC)

- Flexible Tenure: Options ranging from 7 days to 10 years

- Tax Implications: Interest earned is taxable as per your income tax slab

When to Choose FDs: FDs work best for emergency funds, short-term goals (1-3 years), or when you need absolute capital protection. They’re ideal for risk-averse investors who prioritize safety over returns.

Example: If you invest ₹1 lakh in a 1-year FD at 6% interest, you’ll receive ₹1,06,000 after maturity, with ₹6,000 as taxable interest income.

Recurring Deposits (RDs)

Recurring Deposits encourage disciplined saving by requiring you to invest a fixed amount monthly. They’re perfect for building the habit of regular investing while earning slightly better returns than savings accounts.

Mechanism: You commit to depositing a fixed amount every month for a predetermined period. The bank compounds the interest on your accumulated deposits.

Example: Monthly deposit of ₹1,000 for 12 months at 5.5% interest yields approximately ₹12,330 at maturity - your ₹12,000 investment plus ₹330 in interest.

Returns: Typically 3-5% annually, making them suitable for short-term goals and emergency fund building.

Strategic Use: RDs serve as excellent stepping stones to more sophisticated investments like SIPs (Systematic Investment Plans) in mutual funds, helping you develop consistent investment discipline.

Mutual Funds: Professional Money Management

Mutual funds pool money from multiple investors to create diversified portfolios managed by professional fund managers.

Direct Plans: Purchased directly from the fund house, typically through their website or app. These have lower expense ratios as they don’t include distributor commissions, resulting in higher returns over time, hence better choose them.

Regular Plans: Purchased through intermediaries like brokers or financial advisors. While they have higher expense ratios due to commission payments, they may provide valuable advisory services.

Equity Mutual Funds

These funds invest primarily in stocks, offering potential for higher returns but with increased volatility. They’re suitable for long-term wealth creation and beating inflation over time.

Types and Applications:

- Large Cap Funds: Invest in established companies with market capitalization above ₹20,000 crores. They offer stability with moderate growth potential

- Mid Cap Funds: Focus on companies with market cap between ₹5,000-20,000 crores, balancing growth potential with higher risk

- Small Cap Funds: Target companies below ₹5,000 crores market cap, offering highest growth potential but with significant volatility

- Multi-Cap Funds: Provide diversification across all market segments, giving fund managers flexibility to adjust allocations based on market conditions

Tax Efficiency: Equity mutual funds held for more than one year qualify for Long Term Capital Gains (LTCG) tax.

Debt Mutual Funds

Debt funds invest in fixed-income securities like government bonds, corporate bonds, and money market instruments. They’re ideal for investors seeking regular income with lower risk than equity funds.

Categories by Duration:

- Liquid Funds: Invest in instruments with maturity up to 91 days, perfect for parking emergency funds with returns of 4-6%

- Short Duration Funds: Target securities with 1-3 years maturity, suitable for short-term goals

- Medium to Long Duration Funds: Invest in longer-term bonds, potentially offering higher returns but with interest rate risk

Understanding Interest Rate Risk: When interest rates rise, bond prices fall, affecting your fund’s value. Longer-duration funds are more sensitive to interest rate changes. The inverse relationship between interest rates and bond prices exists because of how bonds work. When you buy a bond, you’re essentially lending money to the issuer (like a government or corporation) in exchange for regular interest payments at a fixed rate. For example, imagine you buy a $1,000 bond that pays 3% annually. You’ll receive $30 per year until the bond matures. Now, here’s where interest rate risk comes in. If market interest rates rise to 5%, newly issued bonds will offer this higher rate. Your existing 3% bond suddenly becomes less attractive because investors could buy new bonds paying 5% instead. To compensate for this disadvantage, your bond’s price must fall in the secondary market. Someone would only buy your 3% bond if they could get it at a discount that makes its overall return competitive with the new 5% bonds. The opposite happens when rates fall. If new bonds only pay 2%, your 3% bond becomes more valuable, and its price rises. This price movement affects bond funds directly because they hold many bonds and must mark their portfolio to market daily. When rates rise, the value of all the bonds in the fund falls, reducing the fund’s net asset value (NAV). You experience this as a loss in your fund’s value, even though you haven’t sold anything. Duration measures how sensitive a bond or bond fund is to interest rate changes. It’s expressed in years and roughly tells you how much the bond’s price will change for each 1% change in interest rates. A bond fund with a duration of 5 years would lose approximately 5% of its value if interest rates rose by 1%. Conversely, it would gain about 5% if rates fell by 1%. Longer-duration funds are more sensitive because they typically hold bonds with longer maturities or lower coupon rates. The further into the future a bond’s cash flows extend, the more those future payments are affected by changes in discount rates (interest rates). Think of it this way: a 30-year bond has payments stretching three decades into the future, while a 2-year bond will return your principal relatively soon. The 30-year bond’s price must adjust much more dramatically to remain competitive when rates change. This sensitivity isn’t necessarily bad—it’s simply a characteristic to understand. In falling rate environments, longer-duration funds can provide substantial gains. However, in rising rate environments, they can experience significant losses.

Tax-Saving Mutual Funds (ELSS)

Equity Linked Savings Scheme (ELSS) funds offer the dual benefit of tax savings and wealth creation. They invest predominantly in equity markets while providing tax deductions under Section 80C.

Unique Advantages:

- Tax Deduction: Up to ₹1.5 lakh annual investment qualifies for tax deduction

- Shortest Lock-in: Only 3-year lock-in period among all Section 80C options

- Wealth Creation Potential: Historical returns of 12-15% annually over long periods

- Tax-Efficient Returns: Qualified for LTCG tax treatment after 3 years

Strategic Insight: ELSS funds can serve as your primary equity exposure while simultaneously reducing your tax burden, making them excellent for young professionals in higher tax brackets.

Index Funds and ETFs

Index funds and Exchange Traded Funds (ETFs) track specific market indices, offering broad market exposure at low costs. They represent a passive investment approach, eliminating the need to pick individual stocks or fund managers.

Benefits of Index Investing:

- Low Expense Ratios: Typically 0.1-0.8% compared to 1-2% for actively managed funds

- Broad Diversification: Instant exposure to top companies in an index

- Transparency: You always know exactly what you own

- Consistent Performance: Eliminates manager risk and style drift

ETF Considerations:

- Tracking Error: ETFs may not perfectly track their underlying index due to fees and operational factors

- Liquidity: Can be bought and sold during market hours like stocks

- Minimum Investment: Can start with as little as one unit

Popular ETFs: BeES (Benchmark Exchange Traded Scheme), Nifty ETFs, and sector-specific ETFs.

ETF vs. Index Funds: ETFs trade like stocks on exchanges, allowing intraday buying and selling, while index funds can only be bought/sold at end-of-day prices. Choose ETFs for flexibility and index funds for systematic investing.

International Mutual Funds

These funds invest in global markets, providing geographical diversification and exposure to developed economies. They’re particularly valuable for hedging against domestic market risks and currency fluctuations.

Popular Options:

- US Market Funds: Invest in S&P 500 or broader US indices

- Global Funds: Diversify across multiple countries and regions

- Emerging Market Funds: Focus on developing economies with higher growth potential

Tax Considerations: International funds are taxed as capital gains - gains held for less than 3 years are taxed as per your income slab, while gains beyond 3 years are taxed at 20% with indexation benefits.

Government-Backed Investment Options

Public Provident Fund (PPF)

PPF represents one of India’s most attractive long-term investment options, combining tax benefits with decent returns and complete safety. It’s designed to encourage long-term savings for retirement.

Triple Tax Benefit (EEE):

- Exempt: Investments up to ₹1.5 lakh qualify for tax deduction

- Exempt: No tax on annual interest earned

- Exempt: Maturity amount is completely tax-free

Strategic Features:

- 15-Year Commitment: Minimum tenure builds long-term discipline

- Flexible Contributions: ₹500 minimum to ₹1.5 lakh maximum annually

- Loan Facility: Available from 7th year onwards

- Partial Withdrawal: Allowed from 7th year for specific purposes

Power of Compounding Example: Monthly investment of ₹12,500 (₹1.5 lakh annually) at 7.1% for 15 years grows to approximately ₹40 lakh, with ₹17.5 lakh as tax-free interest.

National Savings Certificate (NSC)

NSC offers a government-guaranteed investment option with a 5-year lock-in period. It’s particularly suitable for conservative investors seeking tax benefits with assured returns.

Features:

- Current Interest Rate: Approximately 6.8% annually (subject to change)

- Tax Benefits: Qualifies for Section 80C deduction

- Automatic Reinvestment: Interest compounds annually

- Transferability: Can be transferred from one person to another

Sukanya Samriddhi Yojana (SSY)

This scheme promotes financial security for girl children through attractive interest rates and comprehensive tax benefits. It’s designed to support education and marriage expenses.

Eligibility and Benefits:

- Age Limit: Girl child aged 0-10 years

- Investment Range: ₹250 minimum to ₹1.5 lakh maximum annually

- Attractive Returns: Currently offering around 7.6% annual interest

- Long-term Maturity: 21 years from account opening

- Partial Withdrawal: Allowed for higher education expenses

Strategic Advantage: SSY currently offers one of the highest government-guaranteed returns available to retail investors, making it an excellent choice for parents planning their daughter’s future.

Government Welfare Schemes

Pradhan Mantri Jeevan Jyoti Bima Yojana (PMJJBY)

A pure term life insurance scheme offering affordable life coverage for low-income families.

Features:

- Coverage: ₹2 lakh life insurance

- Premium: ₹330 per annum

- Age Limit: 18-50 years for entry, coverage up to 55 years

- Tax Benefits: Premiums qualify for tax deduction

- Renewal: Annual renewal required

Pradhan Mantri Suraksha Bima Yojana (PMSBY)

An accident insurance scheme providing affordable coverage against accidental death and disability.

Coverage Details:

- Accidental Death: ₹2 lakh

- Permanent Total Disability: ₹2 lakh

- Permanent Partial Disability: ₹1 lakh

- Premium: ₹20 per annum

- Age Limit: 18-70 years

- Auto-debit: Premium deducted from linked bank account

Pradhan Mantri Awas Yojana (PMAY)

A housing scheme providing interest subsidies for home loans to economically weaker sections.

Eligibility and Benefits:

- Income Limits: Family income up to ₹18 lakh per annum

- Interest Subsidy: 4% to 6.5% depending on income category

- Loan Amount: Subsidies applicable on loan amounts up to ₹9-12 lakh

- Property Value: Varies by city category

Example: A Middle Income Group (MIG-I) buyer with income ₹12 lakh annually buying a ₹50 lakh house gets 4% interest subsidy on ₹9 lakh of the loan amount, with maximum subsidy of ₹2.35 lakh.

Pradhan Mantri Vaya Vandana Yojana (PMVVY)

An immediate annuity scheme for senior citizens providing guaranteed pension for life.

Features:

- Age Limit: 60 years and above

- Pension Options: Monthly, quarterly, half-yearly, or annual pension

- Guaranteed Returns: Currently around 7.4% annually

- Purchase Price: ₹1.5 lakh to ₹15 lakh

- Pension Period: For life of the pensioner

Insurance as an Investment Tool

Understanding insurance requires recognizing its dual nature - protection and investment. While insurance’s primary purpose is risk mitigation, certain products can serve investment goals when chosen wisely.

| Aspect | Term Insurance | Health Insurance | Life Insurance (Traditional / ULIPs) |

|---|---|---|---|

| Purpose | Pure life cover – pays nominee if the insured dies during the policy term | Covers medical expenses and hospitalization | Combines life cover with investment/savings component |

| Coverage | High death benefit (e.g., ₹1 crore) | Hospitalization & treatment costs up to sum insured | Lower life cover + maturity benefit |

| Policy Duration | 10–45 years | 1–3 years (renewable) | 5–30 years |

| Premium Cost | ₹10,000–25,000/year for ₹1 crore cover (age-dependent) | Varies with age, sum insured, and pre-existing conditions | Higher than term plans due to investment component |

| Death Benefit | Full sum assured if death occurs during the term | Not applicable | Life cover + fund value (for ULIPs) or bonus (for traditional plans) |

| Maturity Benefit | None (no return if you survive) | None | Maturity value (returns often 4–6% annualized) |

| Key Benefits | • High coverage at low cost • Financial security for family • Covers liabilities • Tax benefits (Sec 80C) |

• Protection from rising medical costs • Cashless hospitalization • Critical illness cover • Tax benefits (Sec 80D) |

• Enforced savings • Life cover + maturity benefit • Tax benefits (Sec 80C / 10(10D)) |

| Ideal Coverage | 10–15× your annual income | ₹5–10 lakh (individual/family floater) | Often insufficient as standalone life cover |

| Why Choose | Most cost-effective way to protect dependents financially | Healthcare inflation is ~10–15% annually | Only if you seek bundled insurance + disciplined savings |

| Why Be Cautious | N/A | N/A | • High charges (2–3%+ annually) • Complex and less transparent • Lower returns vs. mutual funds • May not provide adequate cover |

| Better Strategy | Buy term insurance for life cover | Buy sufficient health insurance early | Buy term plan + invest separately (e.g., mutual funds) for better flexibility and returns |

Additional Insurance Features:

- MWP (Married Women’s Property Act): Protects insurance proceeds from creditors and family disputes

- Life Stage Benefit: Allows increasing coverage at life milestones

- Zero Depreciation Cover: For vehicle insurance, covers full replacement cost without depreciation

Retirement Planning Instruments

Employee Provident Fund (EPF)

EPF forms the foundation of retirement planning for salaried employees. Both employee and employer contribute, creating a substantial retirement corpus over time.

Contribution Structure:

- Employee Contribution: 12% of basic salary + DA

- Employer Contribution: 12% of basic salary + DA (3.67% to EPF, 8.33% to EPS)

- Tax Benefits: Contributions qualify for Section 80C deduction

- Tax-Free Maturity: Withdrawals after 5 years are tax-free

Compounding Power: EPF currently offers around 8.5% annual returns, compounded annually. A 25-year-old earning ₹50,000 basic salary can accumulate over ₹1.5 crore by retirement through EPF alone.

Employee Pension Scheme (EPS)

EPS is a government-backed pension scheme that works alongside EPF, providing monthly pension after retirement. It’s funded by employer contributions and government support (and not the employee).

Key Features:

| Feature | EPF | EPS |

|---|---|---|

| Employee Contribution | 12% | Nil |

| Employer Contribution | 3.67% | 8.33% |

| Deposit Limit | No predetermined limit | Maximum ₹1,250 per month |

| Age Limit for Withdrawal | Not required | 58 years for regular pension, 50 years for early pension |

| Interest Rate | Interest received is tax-exempt | No interest rate applied |

| Withdrawal of Funds | After 58 years or unemployment for 60+ days | Monthly pension after 58 years |

| Premature Withdrawal | Complete balance can be withdrawn | Amount based on years of service |

EPS Benefits:

- Regular Pension: Monthly pension from age 58 based on years of service and salary

- Early Pension: Available from age 50 with 10 years of service (reduced amount)

- Disability Pension: In case of permanent disability

- Family Pension: For spouse and children after member’s death

- Maximum Pensionable Salary: Currently capped at ₹15,000 per month

Calculation Example: An employee with 35 years of service and average salary of ₹15,000 can expect monthly pension of approximately ₹4,500-5,000.

Atal Pension Yojana (APY)

APY provides guaranteed pension for unorganized sector workers and those not covered by EPF/EPS. It’s a government-backed scheme ensuring basic income security in old age.

Pension Structure:

- Monthly Pension Options: ₹1,000 to ₹5,000 monthly pension

- Entry Age: 18-40 years

- Pension Age: 60 years

- Government Co-contribution: For eligible low-income subscribers

Example: A 25-year-old contributing ₹210 monthly will receive ₹5,000 monthly pension from age 60, with spouse pension and nominee benefits.

Alternative Investment Avenues

Bonds and Debentures

A bond and debenture both are debt instruments used for fund raising. Bonds are issued by the government & debentures by public companies to raise money. Hence bonds are low risk, low reward & debentures high risk, high reward (but it may depend). In simple words; When a company raises money to expand or grow business, they have different methods:

- First, sell their ownership in the form of stocks (but selling ownership continuously is an issue as promoters/key shareholders will lose value)

- Second, Taking a bank loan

- Lastly, Taking loan from public, which is issue of bonds/debentures. Combined bonds from multiple companies is a basically a debt mutual fund.

Government Bonds:

- Issued by: Central and state governments

- Risk Level: Lowest risk as backed by government

- Returns: Lower but guaranteed

- Taxation: Interest taxable as per income tax slab

Corporate Debentures:

- Issued by: Private companies

- Risk Level: Higher risk but potentially higher returns

- Credit Rating: Look for AA or AAA rated instruments

- Priority: Bond holders get priority over shareholders in case of liquidation

Investment Strategy: Focus on high-quality bonds (AA+ or AAA rated) for safety, or consider debt mutual funds for professional management and diversification.

Treasury Bills

Government-issued short-term securities with maturities of 91, 182, or 364 days. They’re considered the safest investment as they’re backed by the government.

How They Work:

- Purchase: Bought at discount to face value

- Maturity: Redeemed at full face value

- Returns: Difference between purchase price and face value

Example: A 91-day treasury bill with face value ₹120 might be available at ₹118.40. After 91 days, you receive ₹120, earning ₹1.60 as risk-free profit.

Sovereign Gold Bonds (SGBs)

SGBs provide exposure to gold prices without the hassles of physical gold storage. They’re issued by the government, ensuring complete safety. Though, as per latest news, they are stopped.

Advantages Over Physical Gold:

- Additional Interest: 2.5% annual interest over gold price appreciation

- No Storage Costs: Eliminates locker charges and insurance

- Tax Benefits: No capital gains tax if held to maturity

- Liquidity: Can be traded on exchanges or held till maturity

Investment Strategy: SGBs work best for long-term gold allocation, typically 5-10% of your portfolio for diversification.

Real Estate Investment Trusts (REITs)

REITs democratize real estate investing by allowing small investors to own shares in large commercial properties. They provide exposure to real estate without the challenges of direct property ownership.

How REITs Work:

- Professional Management: Experienced teams manage properties

- Regular Income: Mandated to distribute 90% of income as dividends

- Liquidity: Trade on stock exchanges like regular stocks

- Transparency: Regular reporting and regulated operations

Types of REITs:

- Office REITs: Invest in office buildings and business parks

- Retail REITs: Own shopping malls and retail properties

- Industrial REITs: Focus on warehouses and logistics facilities

Popular REITs: Embassy Office Parks REIT, Brookfield India Real Estate Trust, Mindspace Business Parks REIT.

Tax Implications: Dividends from REITs are taxable, and capital gains follow equity taxation rules.

Commodity Investments

Commodities provide inflation protection and portfolio diversification. They often perform well when traditional assets struggle.

Major Commodity Exchanges:

- Multi Commodity Exchange (MCX): Largest commodity exchange in India

- National Commodity and Derivatives Exchange (NCDEX): Focus on agricultural commodities

- Intercontinental Exchange (ICE): International commodity platform

- National Multi Commodity Exchange (NMCE): Regional commodity trading

Commodity Categories:

- Metals: Gold, silver, copper, aluminum, zinc

- Energy: Crude oil, natural gas, heating oil

- Agricultural: Wheat, rice, sugar, cotton, spices

- Industrial: Various industrial raw materials

Investment Methods:

- Physical Commodities: Direct ownership of gold, silver

- Commodity ETFs: Exchange-traded funds tracking commodity prices

- Commodity Futures: Leveraged trading in commodity contracts

- Commodity Mutual Funds: Professionally managed commodity portfolios

Real Estate Direct Investment

Key Considerations for Property Investment:

Approved Project Financial (APF) Number: Always verify this unique code before investing. It indicates: Builder’s financial credibility, Government clearances, Dispute-free property status, Faster home loan approval.

Pre-EMI Options: For under-construction properties, consider paying only interest during construction period:

- Advantage: Lower monthly outgo initially

- Disadvantage: Longer total tenure and no immediate tax benefits

- Suitable For: Those paying both rent and EMI simultaneously

Pradhan Mantri Awas Yojana Benefits: Leverage government subsidies for affordable housing to reduce effective interest rates.

Peer-to-Peer (P2P) Lending

P2P lending platforms connect borrowers directly with lenders, potentially offering higher returns than traditional fixed deposits.

How P2P Works:

- Platform Registration: Register with RBI-approved platforms

- Risk Assessment: Platforms evaluate borrower creditworthiness

- Diversification: Spread investments across multiple borrowers

- Regular Returns: Receive monthly payments including principal and interest

Expected Returns: 10-15% annually, significantly higher than FDs but with credit risk.

Risk Management: Never invest more than ₹50,000 per platform (regulatory limit) and diversify across multiple borrowers.

Chit Funds

A traditional savings-cum-loan scheme where contributors pool money monthly, with the total amount auctioned to the lowest bidder each month.

How It Works:

- Group Formation: Fixed number of contributors (e.g., 20 people)

- Monthly Contribution: Each pays fixed amount monthly

- Auction System: Lowest bidder wins the total pool

- Commission: 5% typically goes to organizer

- Surplus Distribution: Remaining amount distributed among non-winners

Example: 20 contributors paying ₹1,000 monthly for 12 months:

- Month 1: Pool = ₹20,000, Winner bids ₹17,000

- Commission: ₹1,000 to organizer

- Surplus: ₹2,000 distributed among 19 others (₹105 each)

- Net Contribution: Others pay only ₹895 in Month 1

Expected Returns: Around 8%, but higher risk due to potential defaults.

Risks: Organizer default, member defaults, and regulatory concerns.

Credit Cards as Financial Tools

Credit cards can be valuable financial instruments when used strategically for rewards and cash flow management.

Benefits of Strategic Credit Card Use:

- Rewards and Points: Earn points on purchases for travel, meals, and shopping

- Cash Flow Management: 45-50 days interest-free credit period

- Purchase Protection: Additional warranty and dispute resolution

- Travel Benefits: Lounge access, insurance coverage, and forex advantages

Credit Card Against Fixed Deposit:

- Secured Credit Cards: Backed by FD as collateral

- Credit Limit: 80-90% of FD amount

- Lower Fees: Reduced charges compared to regular cards

- Easy Approval: Guaranteed approval with FD backing

- FD Benefits: Linked FD continues earning interest

Golden Rules:

- NEVER withdraw cash: Attracts high interest rates immediately

- Pay full amount: Avoid interest charges by paying entire bill

- Use for planned expenses: Don’t overspend just because credit is available

Emerging Investment Opportunities

Cryptocurrency

Digital currencies represent a new asset class with potential for high returns but significant volatility. Indian regulations are evolving, requiring careful consideration.

Key Considerations:

- Regulatory Uncertainty: Tax and legal framework still developing

- High Volatility: Prices can fluctuate dramatically

- Limited Allocation: Consider maximum 5% of portfolio

- Tax Implications: Gains taxed at 30% plus surcharge

Fractional Investing

Technology platforms now allow small investors to buy fractions of expensive stocks, making diversification more accessible.

Benefits:

- Lower Entry Barriers: Own shares of expensive stocks with small amounts

- Better Diversification: Spread investments across more securities

- Systematic Building: Gradually build positions in quality companies

Smallcase Investing

Smallcases offer professionally designed portfolios around specific themes, strategies, or ideas. They provide a middle ground between individual stock picking and mutual fund investing.

Advantages:

- Thematic Exposure: Invest in specific trends or sectors

- Transparency: Know exactly which stocks you own

- Professional Research: Benefit from expert stock selection

- Flexibility: Can modify holdings based on your preferences

Successful investing requires balancing different asset classes based on your age, risk tolerance, and goals.

Technical Ratios and Metrics

Note that, while using these ratios, you have to take into account the company you are analyzing, its industry, and the current market conditions. Ratios can vary significantly across sectors, so always compare with industry averages. We’ll cover fundamental analysis ratios that help evaluate a company or financial instrument’s health, performance, etc. And after that we’ll cover technical analysis ratios (more inclined towards instruments like market stocks).

Stock Metrics

Valuation Ratios

- Price-to-Earnings (P/E) Ratio

- Definition: Indicates how much investors pay for $1 of company earnings.

- Formula:

P/E Ratio = Current Stock Price / Earnings Per Share (EPS) - Types:

- Trailing P/E: Based on past 12 months earnings (historical performance)

- Forward P/E: Based on projected next 12 months earnings (growth expectations)

- Interpretation:

- Industry Average: ~18-20

- Good Range (India): 20-25

- High P/E (>25): May indicate overvaluation or high growth expectations

- Low P/E (<15): May indicate undervaluation or market skepticism

- Always compare with industry P/E for context

- Price-to-Sales (P/S) Ratio

- Definition: Compares market capitalization to total revenue

- Formula:

P/S Ratio = Market Capitalization / Total Revenue - Interpretation:

- Technology/Non-cyclical: <0.75 (highly desirable)

- General stocks: 0.75-1.5 (good picks)

- Above 3: Considered risky

- Industry Average: 1-2

- Particularly useful for companies without profits yet

- Price-to-Book (P/B) Ratio

- Definition: Compares market value to book value of assets

- Formula:

P/B Ratio = Market Price per Share / Book Value per Share - Interpretation:

- Below 1: Potentially undervalued (especially in IT sector)

- Above 1: Investors expect future growth

- Industry Average: <2

- Most relevant for asset-heavy companies like banks and manufacturing

- PEG Ratio (Price/Earnings to Growth)

- Definition: P/E ratio adjusted for earnings growth rate

- Formula:

PEG = P/E Ratio / Annual EPS Growth Rate - Interpretation:

- Below 1: Potentially undervalued relative to growth

- 1-2: Fairly valued

- Above 2: Potentially overvalued

- Helps identify growth stocks at reasonable prices

- Enterprise Value to EBITDA (EV/EBITDA)

- Definition: Total company value compared to operating earnings

- Formula:

EV/EBITDA = Enterprise Value / EBITDA - Interpretation:

- Below 10: Generally attractive

- 10-15: Fair value

- Above 15: Potentially expensive

- Better than P/E for comparing companies with different capital structures

- EV: Enterprise Value = Enterprise Value (EV) represents the total economic value of a company, encompassing both its equity and debt, making it a more comprehensive valuation metric than just market capitalization. It essentially reflects the theoretical cost to acquire the entire company, including paying off its debts.

- Formula: EV = Market Cap + Total Debt - Cash and Cash Equivalents

- Cash and cash equivalents are subtracted from the Enterprise Value (EV) because they represent readily available funds that an acquirer would effectively inherit, reducing the net cost of acquiring the company. Essentially, the cash could be used to pay down existing debt or offset the purchase price, making the company less expensive to acquire.

- EBITDA: Earnings Before Interest, Taxes, Depreciation, and Amortization

- Formula: EBITDA = Operating Income + Depreciation + Amortization

Profitability Metrics

- Return on Equity (ROE)

- Definition: Measures profitability relative to shareholders’ equity

- Formula:

ROE = (Net Income / Shareholders' Equity) × 100 - Interpretation:

- Excellent: >25% (for some industries)

- Good: >15%

- Below 10%: May indicate poor capital efficiency

- Shows how effectively management uses investor capital

- Return on Capital Employed (ROCE)

- Definition: Assesses profitability relative to total capital employed

- Formula:

ROCE = (EBIT / Capital Employed) × 100 - Interpretation:

- Excellent: >20%

- Good: 15-20%

- Below 10%: Poor capital efficiency

- Compare only within same industry

- Return on Assets (ROA)

- Definition: Measures how efficiently assets generate profit

- Formula:

ROA = (Net Income / Total Assets) × 100 - Interpretation:

- Above 5%: Generally good

- Industry-specific: Banks (1-2%), Tech (10%+)

- Indicates asset utilization efficiency

- Profit Margins

- Definition: Percentage of revenue converted to profit at various stages

- Types:

- Gross Profit Margin:

(Gross Profit / Revenue) × 100 - Operating Profit Margin:

(Operating Profit / Revenue) × 100 - Net Profit Margin:

(Net Profit / Revenue) × 100

- Gross Profit Margin:

- Industry Benchmarks:

- Manufacturing: 2-5% net margin

- IT/Software: 18-20% net margin

- FMCG: 10-15% net margin

- Pharmaceuticals: 15-25% net margin

- Higher margins indicate pricing power and efficiency

- EBITDA and EBITDA Margin

- Definition: Earnings Before Interest, Taxes, Depreciation, and Amortization

- Formula:

EBITDA = Net Income + Interest + Taxes + Depreciation + AmortizationEBITDA Margin = (EBITDA / Revenue) × 100

- Interpretation:

- Good EBITDA Margin: >15% for most sectors

- Excellent: >20%

- Useful for comparing companies with different capital structures

- Cash Flow Margin

- Definition: Efficiency in converting sales to operating cash flow

- Formula:

Cash Flow Margin = (Operating Cash Flow / Net Sales) × 100 - Interpretation:

- Strong: >20%

- Good: 10-20%

- Weak: <10%

- Shows actual cash generation capability

Financial Health Indicators

- Debt-to-Equity (D/E) Ratio

- Definition: Measures financial leverage by comparing debt to equity

- Formula:

D/E Ratio = Total Debt / Shareholders' Equity - Interpretation:

- Conservative: <0.5

- Moderate: 0.5-1.5

- Aggressive: >2.0

- Industry context crucial (utilities vs. tech companies)

- Current Ratio

- Definition: Ability to pay short-term obligations with current assets

- Formula:

Current Ratio = Current Assets / Current Liabilities - Interpretation:

- Healthy: 1.2-2.0

- Below 1: Potential liquidity issues

- Above 3: May indicate inefficient asset use

- Basic liquidity indicator

- Quick Ratio (Acid Test)

- Definition: More stringent liquidity measure excluding inventory

- Formula:

Quick Ratio = (Current Assets - Inventory) / Current Liabilities - Interpretation:

- Good: >1.0

- Adequate: 0.7-1.0

- Concerning: <0.5

- Better for companies with slow-moving inventory

- Interest Coverage Ratio

- Definition: Ability to pay interest on outstanding debt

- Formula:

Interest Coverage = EBIT / Interest Expense - Interpretation:

- Safe: >3.0

- Adequate: 1.5-3.0

- Risky: <1.5

- Critical for leveraged companies

- Debt Service Coverage Ratio (DSCR)

- Definition: Ability to service debt including principal and interest

- Formula:

DSCR = Net Operating Income / Total Debt Service - Interpretation:

- Strong: >1.25

- Minimum acceptable: 1.0

- Below 1.0: Cannot cover debt obligations

- Important for lenders and credit analysis

Growth Metrics

- Compound Annual Growth Rate (CAGR)

- Definition: Smoothed annual growth rate over a specified period

- Formula:

CAGR = [(Ending Value/Beginning Value)^(1/n)] - 1 - Interpretation:

- Excellent: >15% over 5 years

- Good: 10-12% (especially for large-cap)

- Market average: 8-10%

- Use for revenue, profit, and other metrics

- Year-over-Year (YoY) Growth

- Definition: Percentage change compared to same period last year

- Formula:

YoY Growth = [(Current Period - Prior Period) / Prior Period] × 100 - Application Areas:

- Revenue growth

- Profit growth

- Volume growth

- Watch for consistency and quality of growth

- Quarter-over-Quarter (QoQ) Growth

- Definition: Sequential quarterly growth rate

- Formula:

QoQ Growth = [(Current Quarter - Previous Quarter) / Previous Quarter] × 100 - Considerations:

- Account for seasonality

- Look for trends over multiple quarters

- More volatile than annual metrics

Cash Flow Metrics

- Free Cash Flow (FCF)

- Definition: Cash available after capital expenditures

- Formula:

FCF = Operating Cash Flow - Capital Expenditures - Interpretation:

- Positive and growing FCF is ideal

- Negative FCF acceptable for growth companies

- Critical for dividends, buybacks, and acquisitions

- Operating Cash Flow to Net Income Ratio

- Definition: Quality of earnings indicator

- Formula:

Operating Cash Flow / Net Income - Interpretation:

- Healthy: >1.0

- Equal to 1: Earnings match cash generation

- Below 1: Potential accounting issues

- Higher ratio indicates better earnings quality

- Free Cash Flow Yield

- Definition: Free cash flow relative to market value

- Formula:

FCF Yield = Free Cash Flow / Market Capitalization - Interpretation:

- Attractive: >5%

- Fair: 3-5%

- Low: <3%

- Alternative to dividend yield

Ownership & Management Metrics

- Promoter Holding

- Definition: Percentage of shares held by company founders/promoters

- Interpretation:

- Strong signal: >50%

- Moderate: 35-50%

- Low: <25% (may indicate lack of confidence)

- Higher holding shows promoter confidence

- Pledged Promoter Holding

- Definition: Promoter shares used as collateral for loans

- Red Flags:

- High pledging: >50% of promoter holding

- Increasing trend: Deteriorating financial situation

- Zero pledging: Ideal scenario

- High pledging indicates financial stress

- Institutional Holding

- Definition: Percentage held by institutional investors

- Categories:

- FII (Foreign Institutional Investors)

- DII (Domestic Institutional Investors)

- Mutual Funds

- Interpretation:

- High institutional holding: >40% shows confidence

- Balanced FII/DII: Better stability

- Indicates professional validation

Efficiency Ratios

- Asset Turnover Ratio

- Definition: Revenue generated per rupee of assets

- Formula:

Asset Turnover = Revenue / Average Total Assets - Interpretation:

- High: Efficient asset utilization

- Industry-specific: Retail (high), Utilities (low)

- Compare within industry only

- Inventory Turnover Ratio

- Definition: How quickly inventory is sold

- Formula:

Inventory Turnover = Cost of Goods Sold / Average Inventory - Interpretation:

- High: Efficient inventory management

- Too high: May indicate stock shortages

- Low: Excess inventory or slow sales

- Critical for retail and manufacturing

- Receivables Turnover Ratio

- Definition: Efficiency in collecting credit sales

- Formula:

Receivables Turnover = Credit Sales / Average Receivables - Days Sales Outstanding:

365 / Receivables Turnover - Interpretation:

- Lower DSO: Better collection efficiency

- Industry norms: Vary significantly

- Important for working capital management

Mutual Fund Analysis

Performance Metrics

- Expense Ratio

- Definition: Annual fee charged for fund management

- Benchmarks:

- Index Funds: <0.5%

- Active Equity Funds: 0.5-0.75% (good)

- Above 1.5%: Considered high

- Direct vs Regular: Direct plans 0.5-1% lower

- Lower expense ratio means higher returns for investors

- Sharpe Ratio

- Definition: Risk-adjusted return measure

- Formula:

Sharpe Ratio = (Fund Return - Risk-Free Rate) / Standard Deviation - Interpretation:

- Excellent: >1.5

- Good: 1.0-1.5

- Average: 0.5-1.0

- Poor: <0.5

- Higher ratio indicates better risk-adjusted performance

- Alpha

- Definition: Excess return over benchmark

- Formula:

Alpha = Fund Return - (Risk-Free Rate + Beta × (Benchmark Return - Risk-Free Rate)) - Interpretation:

- Positive Alpha: Outperforming benchmark

- Zero Alpha: Matching benchmark

- Negative Alpha: Underperforming

- Measures fund manager’s value addition

- Beta

- Definition: Volatility relative to market/benchmark

- Interpretation:

- Beta = 1: Moves with market

- Beta > 1: More volatile than market

- Beta < 1: Less volatile than market

- Negative Beta: Inverse correlation

- Indicates systematic risk exposure

- Standard Deviation

- Definition: Measure of return volatility

- Risk Categories:

- Low Risk: <10%

- Moderate Risk: 10-20%

- High Risk: >20%

- Higher SD means more volatile returns

- Sortino Ratio

- Definition: Risk-adjusted return using only downside deviation

- Formula:

Sortino Ratio = (Return - Risk-Free Rate) / Downside Deviation - Advantage: Focuses only on harmful volatility

- Interpretation: Higher is better, similar scale to Sharpe

Risk Metrics

- Downside Capture Ratio

- Definition: Fund’s performance during market declines

- Formula:

(Fund's negative return / Benchmark's negative return) × 100 - Interpretation:

- Excellent: <80

- Good: 80-90

- Average: 90-100

- Poor: >100

- Lower ratio means better downside protection

- Upside Capture Ratio

- Definition: Fund’s performance during market rallies

- Formula:

(Fund's positive return / Benchmark's positive return) × 100 - Interpretation:

- Excellent: >110

- Good: 100-110

- Average: 90-100

- Higher ratio means better participation in rallies

- Maximum Drawdown

- Definition: Largest peak-to-trough decline

- Formula:

(Trough Value - Peak Value) / Peak Value × 100 - Interpretation:

- Shows worst-case scenario

- Compare with peers and benchmark

- Important for risk assessment

- Tracking Error

- Definition: Standard deviation of excess returns vs benchmark

- Formula:

Standard Deviation of (Fund Return - Benchmark Return) - For Index Funds:

- Excellent: <0.5%

- Good: 0.5-1%

- Poor: >2%

- Lower is better for passive funds

Portfolio Metrics

- Portfolio Turnover Ratio

- Definition: Frequency of portfolio changes

- Formula:

(Lesser of Purchases or Sales) / Average AUM × 100 - Interpretation:

- Low (<50%): Buy-and-hold strategy

- Moderate (50-100%): Balanced approach

- High (>100%): Active trading

- Higher turnover means higher transaction costs

- Asset Under Management (AUM)

- Size Categories:

- Very Large: >₹10,000 Cr

- Large: ₹5,000-10,000 Cr

- Medium: ₹1,000-5,000 Cr

- Small: <₹1,000 Cr

- Implications:

- Too large may face liquidity issues

- Too small may have higher expense ratios

- Optimal size depends on strategy

- Size Categories:

- Exit Load

- Definition: Fee for early redemption

- Typical Structure:

- 1% if redeemed within 12 months

- 0.5% if redeemed within 6 months

- Nil after specified period

- Lower exit load provides more flexibility

- Cash Holdings

- Definition: Percentage of portfolio in cash/equivalents

- Interpretation:

- Normal: 2-5%

- High (>10%): Defensive positioning

- Very Low (<2%): Fully invested

- Indicates fund manager’s market view

Insurance Sector Metrics

Life Insurance Metrics

- Claim Settlement Ratio (CSR)

- Definition: Percentage of claims settled vs. received.

- Formula:

CSR = (Claims Settled / Total Claims) × 100 - Benchmarks: Excellent: >95%, Good: 90–95%, Concerning: <90%

- Higher CSR indicates reliable insurer

- Claim Rejection Ratio

- Definition: Percentage of claims rejected.

- Benchmarks: Good: <2%, Acceptable: 2–5%, High: >5%

- Lower is better for policyholders

- Amount Settlement Ratio

- Definition: Percentage of claimed amount actually paid.

- Formula:

(Total Amount Paid / Total Amount Claimed) × 100 - Benchmarks: Excellent: >95%, Good: 90–95%, Poor: <90%

- Shows partial settlement practices

- Solvency Ratio

- Definition: Indicates an insurer’s ability to meet long-term liabilities.

- Regulatory Minimum: 1.5

- Benchmarks: Strong: >2.0, Adequate: 1.5–2.0, Concerning: Near 1.5

- Higher ratio indicates financial strength

- Persistency Ratio

- Definition: Measures how many policies are renewed over time.

- Time Frames: 13th month (1st year), 25th month (2nd year), 61st month (5th year)

- Good Persistency:

- 13th month: >80%

- 61st month: >50%

- Indicates customer satisfaction

- Incurred Claim Ratio (ICR)

- Definition: Claims paid as percentage of premiums

- Formula:

(Claims Incurred / Premiums Earned) × 100 - For Health Insurance: Optimal: 60-90%, Too Low (<50%): Overpriced policies, Too High (>100%): Unsustainable

- Balance between value and sustainability

Health Insurance Considerations

- Network Hospitals: Look for wide and accessible network. Pan India: 5000+ hospitals preferred & 500+ hospitals in tier 1 city.

- Pre-existing Disease Waiting Period: Standard Periods: General: 2-4 years, Specific Conditions: May vary.

- Pre/Post Hospitalization: Minimum 30 days before and 60 days after

- Day Care Procedures: Should cover treatments requiring <24 hrs admission

- No Claim Bonus (NCB): Typically 10–50% increase in coverage for claim-free years

- Co-payment Clause: Lower % is better for policyholder

- Room Rent Limits: Preferably no sub-limits (flexibility in hospital choice)

- Incurred Claim Ratio (ICR): Balanced range: 60–90%

- Complaint Volume: Check IRDAI annual report or website

- Cashless Claim Settlement Time: Ideal: Less than 2 hours. Faster settlement reduces financial stress

Technical Analysis for Trading

Trend Indicators

- Moving Averages

- Definition: Price averages over specific periods to identify trends

- Types:

- Simple Moving Average (SMA): Equal weight to all prices in period

- Exponential Moving Average (EMA): More weight to recent prices, faster response

- Weighted Moving Average (WMA): Linear weight distribution favoring recent data

- Displaced Moving Average (DMA): MA shifted forward/backward in time

- Double Exponential Moving Average (DEMA): Reduced lag for faster signals

- Key Periods:

- 20 DMA: Short-term trend (approximately 1 month)

- 50 DMA: Medium-term trend (approximately 2.5 months)

- 200 DMA: Long-term trend (approximately 200 trading days/year)

- Trading Signals:

- Price above MA: Uptrend confirmation

- Price below MA: Downtrend confirmation

- Golden Cross: 50 DMA crosses above 200 DMA (bullish)

- Death Cross: 50 DMA crosses below 200 DMA (bearish)

- Best used in trending markets, less effective in sideways markets

- MACD (Moving Average Convergence Divergence)

- Definition: Momentum indicator showing relationship between two moving averages

- Components:

- MACD Line: 12-period EMA minus 26-period EMA

- Signal Line: 9-period EMA of MACD line

- Histogram: MACD line minus Signal line (visualizes convergence/divergence)

- Trading Signals:

- MACD crosses above signal line: Bullish momentum

- MACD crosses below signal line: Bearish momentum

- Zero line crossovers: Trend confirmation (above = bullish, below = bearish)

- Divergences: Price makes new high/low but MACD doesn’t (reversal signal)

- Most effective in trending markets, prone to whipsaws in ranging markets

- Average Directional Index (ADX)

- Definition: Measures trend strength without indicating direction

- Range: 0-100 scale

- Interpretation:

- Above 25: Strong trend present

- 20-25: Developing trend

- Below 20: Weak or no trend (ranging market)

- Above 40: Very strong trend

- Often combined with +DI and -DI lines for direction

- Does not indicate trend direction, only strength

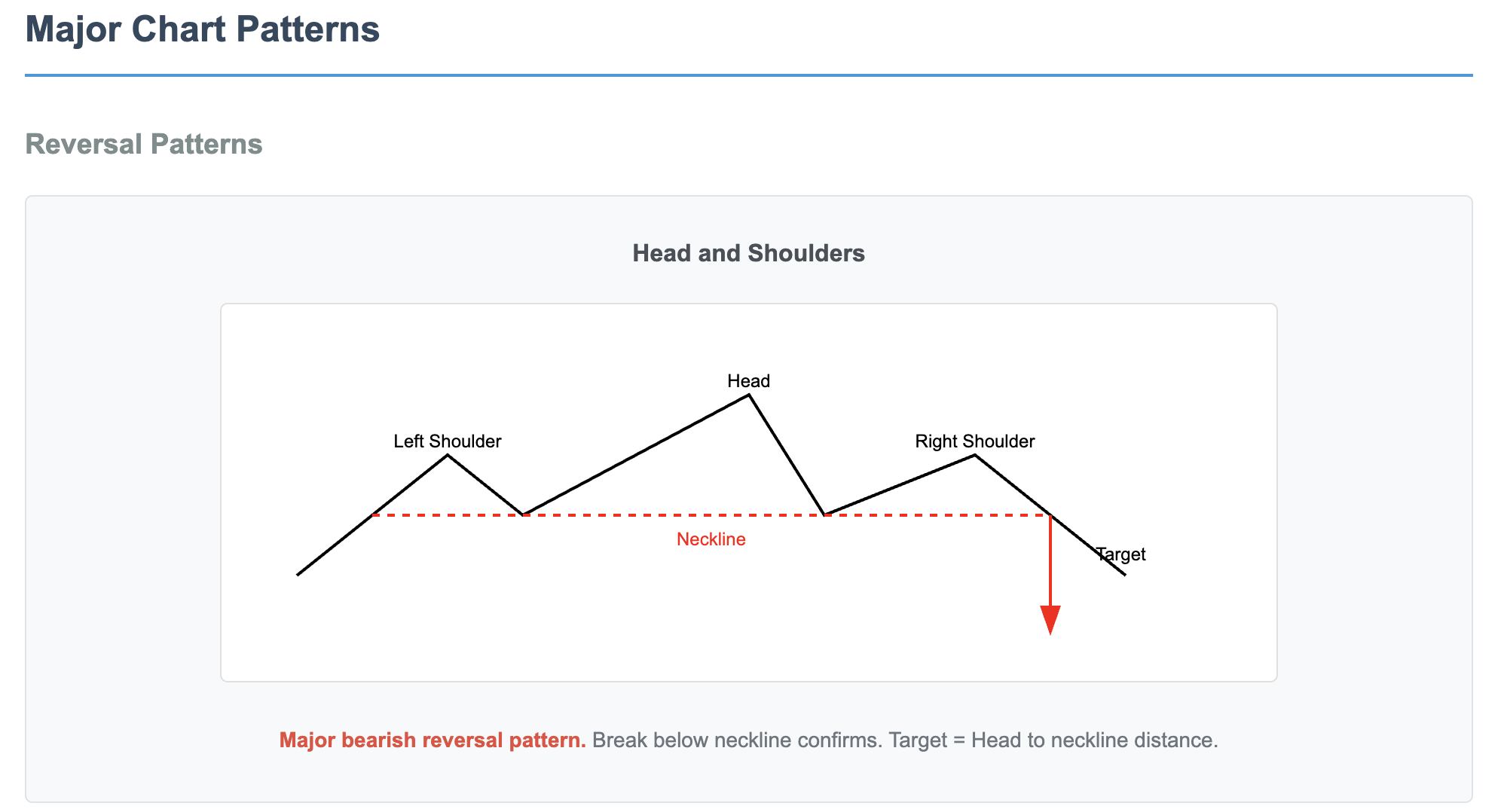

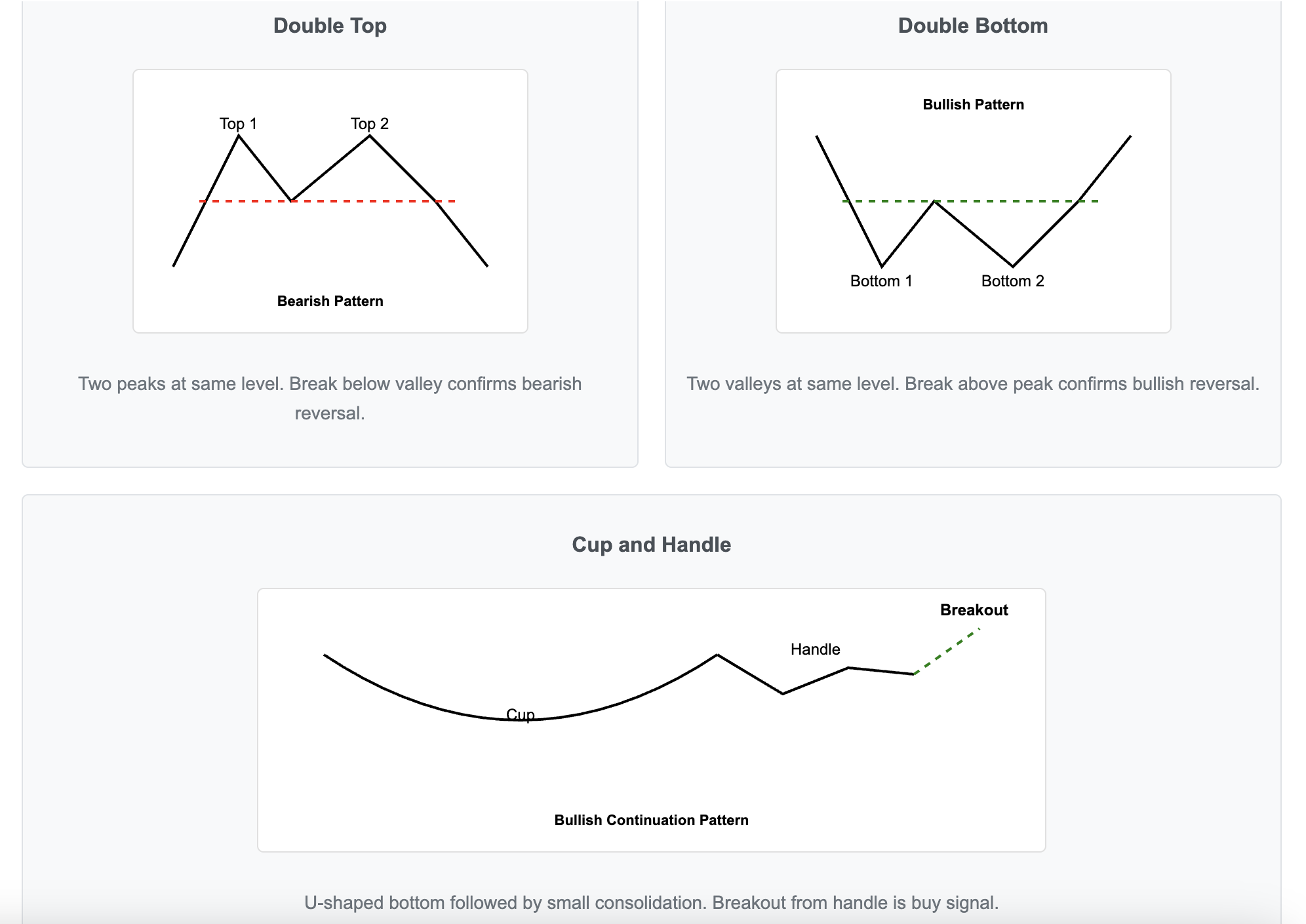

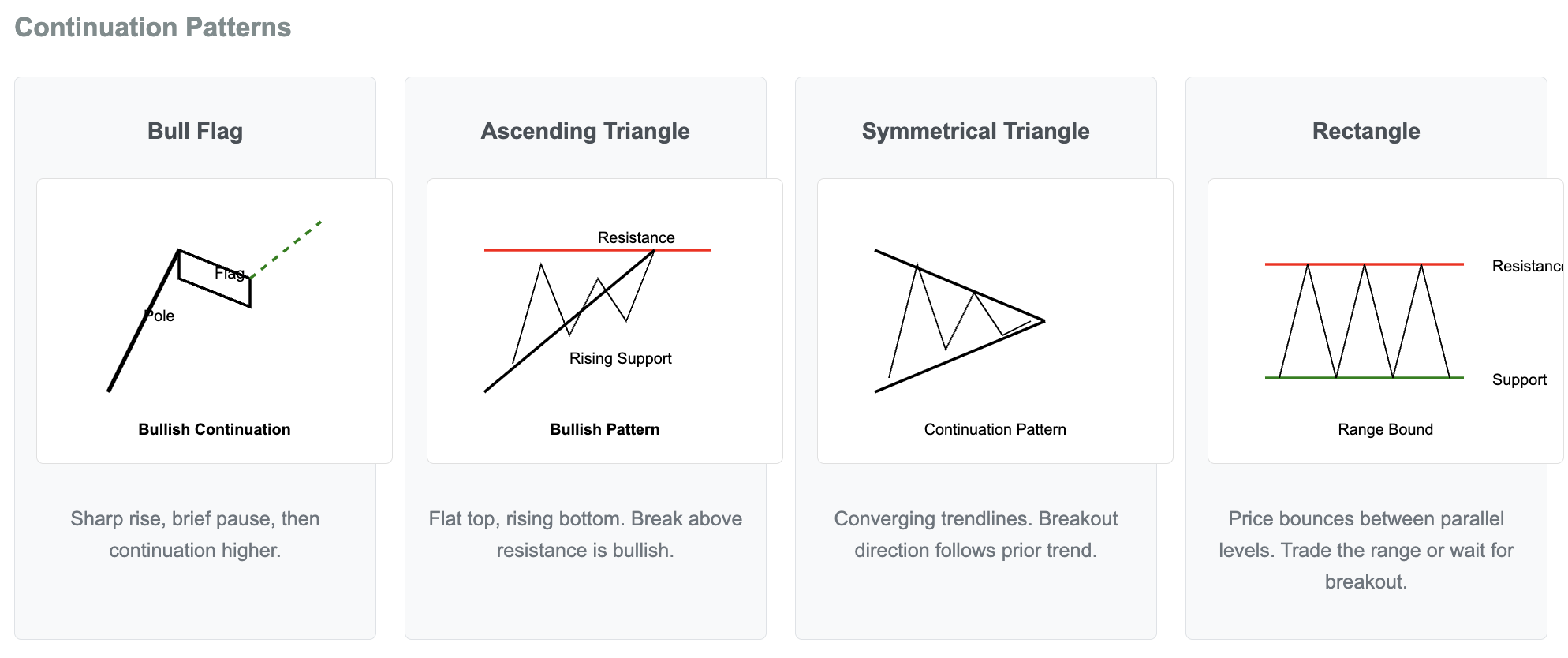

- Support and Resistance Levels

- Support: Price level where buying interest prevents further decline

- Acts as price floor